What is a Blockchain and how does it work?

What is a blockchain?

Blockchain is a decentralised and distributed digital ledger technology used to record transactions. It operates as a chain of blocks, with each block containing a set of transactions. These blocks are linked together sequentially in a chronological order, creating a secure and transparent record of transactions.

Decentralisation within the context of blockchain refers to the principle of distributing control and decision-making authority across the network's users, rather than relying on a single entity, such as a government or corporation. This approach is beneficial in scenarios where individuals need to coordinate with strangers or ensure the security and reliability of their data.

In a decentralised blockchain network, there is no central authority or intermediary that exercises control over data or transactions. Instead, the validation and recording of transactions are carried out by a dispersed network of computers collaborating to uphold the network's integrity.

When people discuss blockchain technology, they are often referring to more than just the underlying database. This technology powers applications like cryptocurrencies and non-fungible tokens (NFTs), enabling individuals to collaborate and engage in transactions without depending on a central governing body.

How does blockchain work?

At its essence, a blockchain is a secure digital ledger that records transactions between two parties in an unalterable manner. This recording process involves a network of specialised computers, known as nodes, distributed globally.

When a user initiates a transaction, such as transferring cryptocurrency to another user, it is broadcasted to the network. The transaction is then authenticated by each node, which verifies digital signatures and other relevant data.

Once validated, the transaction is added to a block alongside other verified transactions. These blocks are interconnected using cryptographic techniques, creating the blockchain. The verification and addition of transactions are achieved through a consensus mechanism, a set of rules guiding how nodes on the network reach agreement on the blockchain's state and transaction validity.

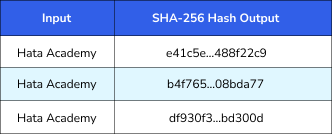

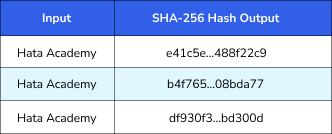

Cryptography plays a critical role in maintaining the security, transparency, and tamper resistance of the blockchain's transaction records. For instance, one important cryptographic method used is hashing, which converts input data of any size into a fixed-size string of characters.

The hash functions employed in blockchains are designed to be collision resistant, making it highly improbable to find two pieces of data that produce the same output. Additionally, they exhibit the avalanche effect, where even minor changes in input data yield vastly different outputs.

Consider the example of SHA256, a function used in Bitcoin, where altering the capitalisation of letters drastically changes the output. Hash functions are also one-way, making it computationally infeasible to reverse-engineer the input data from the hash output.

Each block in a blockchain contains a secure hash of the previous block, forming a strong chain of interconnected blocks. Modifying a single block would necessitate altering all subsequent blocks, which is a technically challenging and prohibitively expensive task.

Public-key cryptography, also known as asymmetric cryptography, is another widely used cryptographic method in blockchains. It facilitates secure and verifiable transactions between users.

Here's how it works: Each participant possesses a unique pair of keys – a private key kept secret and a public key shared openly. When initiating a transaction, a user signs it using their private key, creating a digital signature.

Other users on the network can then verify the transaction's legitimacy by using the sender's public key to authenticate the digital signature. This ensures secure transactions, as only the legitimate owner of the private key can authorise a transaction, while everyone can verify the signatures using the public key.

Transparency is another notable aspect of blockchain. Anyone can generally inspect the data within the blockchain on public blockchain sites, including transaction data and block information. For instance, blockchain explorer sites for Bitcoin allow users to view every recorded transaction, including sender and receiver identifiers, transfer amounts, and a list of bitcoin owners. Moreover, users can trace blocks from the present back to the very first block, known as the genesis block.

What is a consensus mechanism?

A consensus algorithm is a method that facilitates coordination among users or machines in a distributed environment. Its primary goal is to ensure that all participants in the system can unanimously agree on a single and accurate version of the truth, even if certain agents encounter failures. These algorithms are crucial for blockchains because they establish a unified ledger across all network nodes, enabling the recording and verifying of all transactions without the need for a central authority.

In a blockchain network where tens of thousands of nodes maintain copies of blockchain data, certain challenges may arise, such as data consistency and the presence of malicious nodes. To address these issues and maintain the integrity of the blockchain, various consensus mechanisms are employed to govern how network nodes reach a consensus. Let's now delve into the main ones.

Types of consensus mechanisms

1. What is Proof of Work?

Proof of Work (PoW) is a consensus mechanism utilised in numerous blockchain networks to authenticate transactions and preserve the blockchain's integrity. It is the original consensus mechanism employed by Bitcoin.

In the PoW system, miners engage in competition to solve a sophisticated mathematical problem, aiming to be the first one to add the next block to the blockchain. This process, commonly referred to as mining, rewards the successful miner with cryptocurrency.

To mine new coins and ensure network security, miners are required to utilise powerful computers to solve these mathematical problems. As a result, the mining process demands significant computational power and, consequently, consumes a substantial amount of energy.

2. What is Proof of Stake?

Proof of Stake (PoS) is a consensus mechanism developed to address some of the limitations of Proof of Work (PoW). Unlike PoW, where miners compete to solve intricate mathematical problems for transaction validation and block addition, PoS employs a different approach.

In the PoS system, the process of transaction validation and block creation involves validators who are chosen based on the amount of cryptocurrency they hold as collateral or "stake" in the network. These validators are randomly selected, with the size of their stake influencing their chances of being chosen.

Validators are incentivised to act in the network's best interest, as they are rewarded with transaction fees for creating new blocks. Their stake serves as a guarantee of their commitment to the network's integrity and security. This mechanism aims to reduce energy consumption and enhance efficiency compared to PoW.

3. Other popular consensus mechanisms

Proof of Work and Proof of Stake are well-known consensus algorithms, but there exist several others, including hybrid approaches that combine attributes from both systems, as well as entirely distinct methods.

An example of a hybrid algorithm is Delegated Proof of Stake (DPoS), which resembles PoS. However, in DPoS, instead of all validators having the opportunity to create new blocks, token holders elect a smaller group of delegates to perform this task on their behalf.

On the other hand, Proof of Authority (PoA) consensus mechanisms enable validators to be chosen based on their reputation or identity, rather than the amount of cryptocurrency they possess. Validators are selected for their trustworthiness, and if they behave maliciously, they can be removed from the network entirely.

Benefits of Blockchain

1. Decentralisation

The inherent decentralisation of blockchain ensures that there is no central point of control or vulnerability on its network, which enhances its security and resilience against attacks or data breaches.

2. Transparency

In a blockchain, all participants have the ability to view transactions, which simplifies the process of tracking, verifying, and ensuring the accuracy of these transactions.

3. Immutability

Once a transaction is recorded on a blockchain, it becomes immutable and cannot be altered or deleted. This creates a permanent and verifiable record of all transactions that is accessible to anyone within the blockchain network. This differs from traditional systems where transactions are reversible.

4. Efficiency

Blockchain facilitates quicker and more efficient transactions by eliminating the need for intermediaries like banks.

5. Lower Fees

By removing intermediaries and automating processes, blockchain can reduce transaction costs and improve the efficiency of certain business operations.

6. Trust Lessness

Blockchain technology enables transparent transactions that are verified and validated direct;ly by the network's participants, eliminating the need for trusted intermediaries.

What are the different types of blockchain networks?

1. Public blockchain

A public blockchain is a decentralised network that encourages participation from anyone. These networks are typically open source, transparent, and permissionless, allowing anyone to access and utilise them. Examples of public blockchains include Bitcoin and Ethereum.

2. Private blockchain

A private blockchain, as its name implies, is a blockchain network with limited access and not open to the public. These networks are typically controlled by a single entity, like a company, and are utilised for internal purposes and specific use cases.

Private blockchains operate within permissioned environments with defined rules governing who can access and contribute to the chain. They are not fully decentralised systems as there is a clear hierarchical control structure. However, they can be distributed in the sense that multiple nodes maintain copies of the chain on their machines.

3. Consortium blockchain

A consortium blockchain combines features of both public and private blockchains. It involves multiple organisations collaborating to establish a shared blockchain network that is collectively managed and governed. The openness or closed nature of the network depends on the consortium members' requirements.

In a consortium blockchain, a specific and equally influential group of entities functions as validators. This differs from open systems where any individual can validate blocks, or closed systems where a single entity assigns block producers.

The rules of the consortium blockchain are adaptable, permitting various degrees of visibility. The blockchain's visibility can be restricted solely to validators, authorised individuals, or open to all. When validators achieve a consensus, changes can be easily implemented. As long as a certain proportion of these participants act in good faith, the system remains stable without facing challenges.

What is blockchain used for?

Although blockchain technology is relatively young, it has already found applications across various industries. Some of the most prominent current use cases of blockchain technology include:

1. Cryptocurrencies

The primary objective behind developing blockchain technology was to facilitate the creation of cryptocurrencies, utilising it as a secure and decentralised ledger for recording transactions.

2. Digital identity

Blockchain holds the potential to establish secure and unalterable digital identities, enabling the verification of personal information and other sensitive data. As more of our personal information and assets move into the online space, this capability could become more significant.

3. Voting

Blockchain technology can be utilised to develop a secure and transparent voting system by offering a decentralised and unchangeable ledger of all cast votes. This approach eliminates the risk of voter fraud and guarantees the integrity of the voting process.

4. Supply chain management

Blockchain technology enables the creation of a supply chain ledger, where each transaction is recorded as a block on the blockchain. This approach establishes an unchangeable and transparent record of the entire supply chain process.

5. Smart contracts

Smart contracts are automated contracts that self-execute when specific conditions are fulfilled. With blockchain technology, smart contracts can be created and executed securely in a decentralised manner. One of the most promising uses of smart contracts is for Decentralised Applications (dApps) and Decentralised Autonomous Organisations (DAOs).

In summary

Blockchain technology offers a secure and transparent approach for recording transactions and storing data, potentially elevating trust and security in the digital realm, and potentially revolutionising various industries.

From enabling peer-to-peer transactions and creating novel digital assets to facilitating decentralised applications, blockchain technology presents numerous possibilities. As the technology continues to evolve and gain broader acceptance, we can anticipate the emergence of additional innovative and transformative use cases in the coming years.

DISCLAIMER & WARNING

The information provided here is presented "as is'' and is intended for general informational and educational purposes only. It does not come with any representation or warranty of any kind. This content should not be interpreted as financial, legal, or other professional advice, and it is not intended to endorse or recommend the purchase of any specific product or service. It is advisable to consult with appropriate professional advisors for personalized guidance. In cases where the article is contributed by a third-party author, please note that the expressed views belong to the author alone and may not necessarily reflect the opinions of Hata. For further details, we encourage you to read our complete disclaimer. Please be aware that the prices of digital assets can be highly volatile. The value of your investment may increase or decrease, and there is a risk that you may not recover the full amount invested. You are solely responsible for making your own investment decisions, and Hata cannot be held liable for any losses you may incur. This material is not to be construed as financial, legal, or other professional advice. For more information, please refer to Hata’s Terms of Use and Risk Warning.

In a nutshell;

Blockchain functions as a distributed digital ledger, ensuring the secure recording of transaction data across numerous specialised computers connected on the network.

The immutability of blockchain is guaranteed by utilising cryptography and consensus mechanisms. This means that once data is recorded, it becomes permanently unchangeable.

Blockchain serves as the fundamental technology behind cryptocurrencies such as Bitcoin and Ethereum, playing a crucial role in promoting transparency, security, and confidence in various industries beyond the financial sector.

Company

Explore

Legal

Contact Us

49, Jalan Dungun, Bukit Damansara, 50490 Kuala Lumpur, Malaysia.

Copyright ©2026 Hata. All rights reserved.

Compliance